The Elements of Innovation Discovered

The Elements of Innovation Discovered

Metal Tech News - February 19, 2024

China controls most of the resources and processing of energy transition minerals, such as rare earths and lithium, both of which have been discovered in the geothermal depths of the Salton Sea in California, shifting the balance of power and influence over global lithium supply.

Revitalizing the Salton Sea: what began as a long-abandoned, decaying tourist trap is becoming an emerging wetland sanctuary and the site of the world's largest source of green lithium.

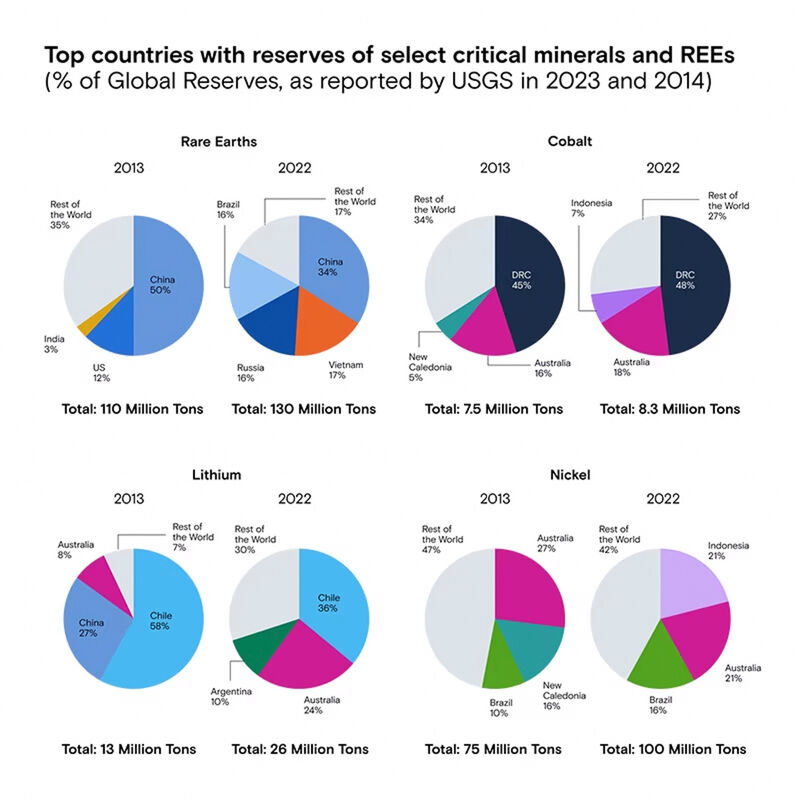

Comparative USGS Mineral Commodity Summaries between 2013 and 2022 demonstrate the impressive fluctuation of global reserves as the search for critical minerals goes on.

There's a new international race, not into space or to establish military superiority, but to secure critical minerals in a worldwide resource grab for the feedstocks that will fuel a global green energy transition.

While we're all on the same side – or, in this case, the same planet – the superpowers have been at odds with how to achieve net-zero carbon emissions and arrest global warming. Underlying it all is a morass of political differences, uneven natural resource distribution, and, of course, money.

During World War I, the U.S. developed its initial list of critical minerals that included nickel, nitrates, platinum, tin, and potash, which had become scarce within the first few years of the conflict.

Over this last decade, the adoption of the Paris Agreement, a global pandemic, and Russia's invasion of Ukraine have all demonstrated the U.S. still has a tenuous hold on a growing list of key minerals.

According to Goldman Sachs' Jared Cohen, "In the last five years, the critical minerals market doubled in size, to $320 billion, and is forecast to double again before the end of the decade. But even these rapidly growing figures understate the importance of the industry, as nearly every piece of technology used in daily life and business requires critical mineral inputs."

As world powers continue to lay claim to mineral reserves around the globe, resource-rich countries are employing protectionist measures to further secure their own green energy supply chains.

While about half of all known rare earth element (REE) deposits were located in China ten years ago, that has decreased to approximately one-third after the discovery of new deposits, driving the communist nation's broader control of supply down from 97% to 63%.

Meanwhile, last November's revised estimate of lithium in California's Salton Sea represents what is now believed to be the world's largest reserve (more than 3.4 million tons) and a significant shift in U.S. influence over global lithium supply.

Revitalizing the Salton Sea: what began as a long-abandoned, decaying tourist trap is becoming an emerging wetland sanctuary and the site of the world's largest source of green lithium.

The lithium discovered is worth approximately $540 billion, the equivalent of supplying a lithium battery to every U.S. vehicle currently on the road as well as to "meet or exceed global lithium demand for decades." Additionally, lithium extraction from the Salton Sea can be done in an environmentally safer manner than traditional methods employed in China.

These massive reserves give the U.S. a much-needed sense of domestic control over the namesake mineral in lithium-ion batteries powering electric vehicles and storing electricity at the grid scale.

With strategic foresight, China has developed significant economic sway in critical minerals processing and EV battery manufacturing, leaving the West heavily dependent on the Middle Kingdom and scrambling to recover some semblance of self-reliance and supply chain security.

China's recent export controls on graphite hearken to past coercive rare earths trade practices toward Japan in 2010, while Australia has also chafed against similar restrictions from 2019 onward, coinciding with the Chinese government's stated grievances with AU political alliances, actions, and policy decisions.

The expanding trend of "friend-shoring" – in which countries shift and diversify strategic links across supply chains to incorporate friendly nations – has developed from growing concerns regarding access to and ownership of critical minerals as a national security priority.

Markets and reserves for cobalt, copper, lithium, nickel, REEs and other critical minerals have seen a lot of action as anticipated and real demand grows for EVs and renewable energy technologies in addition to the usual production of consumer and military goods from phones to fighter jets. This demand is further influenced by various industry leaders' and countries' self-imposed emissions reduction promises and deadlines.

International trade is a two-way street; China produces more than it needs and must sell its goods somewhere. The U.S. also exports to China – its largest percentage of goods being soybeans and grains, as well as semiconductors and services from banking to insurance.

In October 2022, U.S. trade controls on exporting semiconductor chips, sophisticated manufacturing equipment and related expertise demonstrated that neither country is above exerting economic pressures to manipulate markets. Like the U.S. with critical minerals, China will continue its efforts to become self-reliant in semiconductor production and the like. Supply chains can be reorganized over time, moving chokepoints to allied countries.

These actions inevitably result in retaliatory constraints on the export of tech components destined for the U.S. China announced in early July of 2023 that it would restrict the export of gallium and germanium, which are fundamental to building U.S. communications equipment, defense systems, electronics, and space technologies.

"Our mineral import dependence continues to be a gaping hole in our economic and national security and we're clearly not moving fast enough to course correct," said National Mining Association President and CEO Rich Nolan after the 2024 release of USGS Mineral Commodity Summaries. "From electrification and grid transmission buildout to infrastructure and transportation needs, mineral demands are going vertical while mine approvals are at a standstill and unnecessary land withdrawals are taking mineral access in the wrong direction."

Comparative USGS Mineral Commodity Summaries between 2013 and 2022 demonstrate the impressive fluctuation of global reserves as the search for critical minerals goes on.

Despite this, the U.S. has struggled to secure its own domestic resources, still dragging its feet on opportunities to expand domestic mines in resource-rich states like Alaska.

Per an analysis of global trade data published in the International Security academic journal, China has its own dependence on the U.S. and allies for goods ranging from luxury items to raw materials needed for industry.

Rival trade policies will continue to counter (and create) economic pressure applied to specific nations in the networks of interdependence created by globalization. As a result, several nations burned by such practices have been developing measures to identify economic security vulnerabilities and facilitate trade diversification.

The Australia-United States Taskforce on Critical Minerals was formed in 2023 to "deepen the bilateral collaboration on the critical minerals and materials that are vital to clean energy as well as defense supply chains," according to a White House press release.

Several like-minded institutions have arisen, such as the Quadrilateral Security Dialogue (or Quad) – an informal democratic alliance between the U.S., Australia, India, and Japan – which initially grew out of maritime cooperation after the Indian Ocean tsunami of 2004 – and is being strengthened by continued cooperation across security, economic, and health issues such as COVID-19 vaccine development, climate change remediation and now supply-chain resilience.

Similarly, the Indo-Pacific Economic Framework, including the Quad countries along with Brunei Darussalam, Fiji, Indonesia, the Republic of Korea, Malaysia, New Zealand, Singapore, the Philippines, Thailand, and Vietnam, was launched in May 2022 to advance resilience, sustainability, inclusiveness, economic growth, and competitiveness for these interconnected economies.

The U.S.-led Minerals Security Partnership (MSP) is the latest collaboration that includes Australia, Canada, Finland, France, Germany, India, Italy, Japan, Norway, Sweden, South Korea, the UK and others. The partnership was created for international cooperation between governments and industry to facilitate ESG and support strategic projects along an international green energy value chain. (Since 2023, Argentina has been in conversations with the MSP, insinuating a special cooperation deal for Argentine minerals from the Lithium Triangle.)

The U.S. is beginning to push the needle regarding its own net-zero strategy with policies like the Inflation Reduction Act (IRA), disqualifying components by foreign entities of concern (namely organizations under the control of China, North Korea, Russia, or Iran) from being eligible for subsidized purchase by American consumers.

The struggle to develop a robust domestic critical minerals industry is twofold: securing resources as well as developing home-grown processing and manufacturing capacity.

Supply chains are complex and require significant investments of time, expertise, and funds to develop. Increased diversification this last decade in the sourcing of critical minerals has been counteracted by the nominal development of local processing capabilities.

Building new processing facilities is less expensive and time-consuming than constructing new mines but with similar permitting hurdles as well as environmental and social concerns over water use, emissions, contamination, and waste.

Emerging policies are being adopted by several countries in tandem to secure supply chains through reshoring – retaining domestic supply, and friend-shoring – redistributing exports to friendly economic partners. These measures are designed to reduce overdependence on any one country and minimize vulnerability to economic coercion.

A wave of government interventions has been created with the IEA Critical Minerals Policy Tracker https://www.iea.org/reports/introducing-the-critical-minerals-policy-tracker/ensuring-supply-reliability-and-resiliency identifying a range of nearly 200 policies and regulations across the globe, more than half of which were enacted in the past few years.

A sampling beyond the IRA in the U.S. includes the EU's Critical Raw Materials (CRM) Act, Australia's Critical Minerals Strategy and Canada's Critical Minerals Strategy, among others.

Reader Comments(0)