The Elements of Innovation Discovered

The Elements of Innovation Discovered

Metal Tech News – August 16, 2023

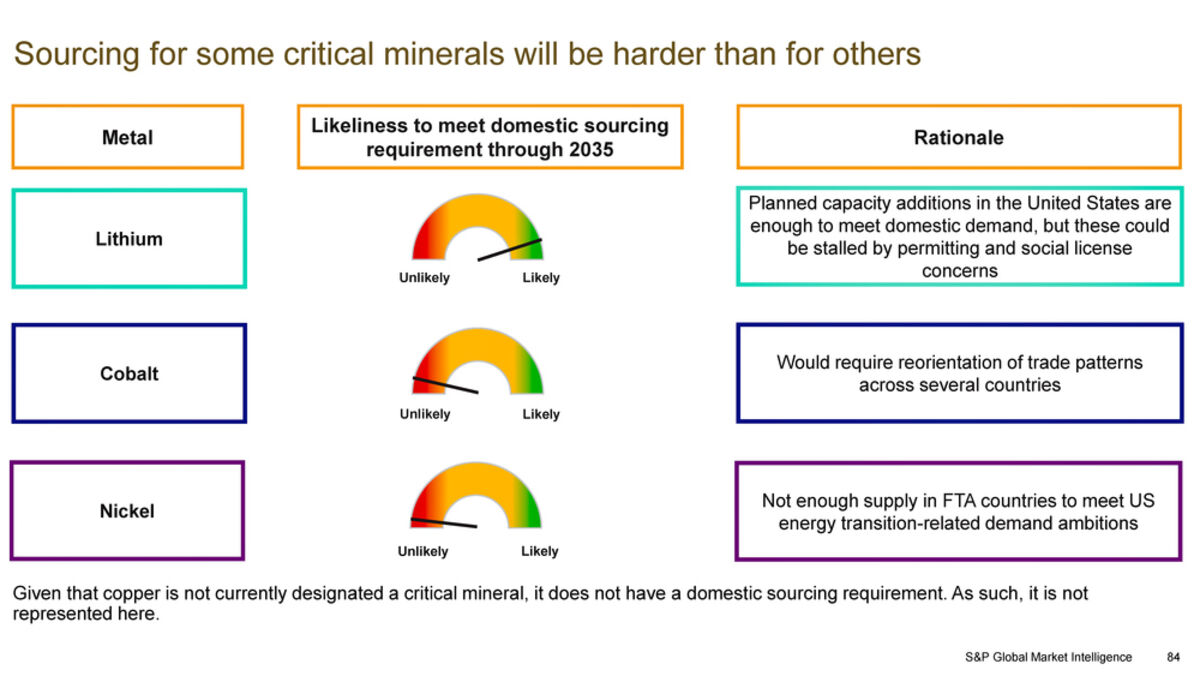

S&P Global analysts forecast the U.S. will likely have adequate supplies of lithium that meets Inflation Reduction Act sourcing requirements but not enough cobalt or nickel.

S&P Global Vice Chairman Daniel Yergin and Alaska Gov. Mike Dunleavy discuss Alaska's role in America's energy transition during the 2023 Alaska Sustainable Energy conference.

The United States has "considerable challenges" to overcome when it comes to securing enough critical minerals and copper to meet the increased energy transition-related demands being driven by the Inflation Reduction Act, according to analysis by S&P Global.

Detailed in a new 111-page report – Inflation Reduction Act: Impact on North America Metals and Minerals Market – this study found that energy transition technologies such as electric vehicles, charging infrastructure, solar, wind, and batteries are adding a substantial boost to the already surging U.S. demand for lithium, cobalt, nickel, and copper.

With the lift from the IRA, the total demand for lithium, nickel, and cobalt will be 23 times higher in 2035 than it was in 2021, and the demand for copper will double over the same span. Adding to the challenges to meeting this demand, energy transition minerals must be mined or processed in the U.S. or a free trade agreement country – and cannot involve a "foreign entity of concern" – in order to qualify for tax credits offered by the IRA.

S&P Global analysts forecast that lithium will be the only one of the four energy metals that will be sufficiently supplied to the United States under the IRA's domestic content requirements, based on already-planned new supplies in the U.S. and free trade agreement countries such as Australia, Canada, and Chile.

"This new comprehensive analysis shows that the Inflation Reduction Act is indeed transformative on the demand side," said S&P Global Vice Chairman Daniel Yergin. "However, challenges remain in securing supply of critical minerals needed to meet growing demand and achieve its goal of accelerating the energy transition."

One of the key challenges for the U.S. is a permitting timeline that is much too long to fit within the clean ambitions set by the White House and supported by the IRA.

"Timely and transparent permitting is a fundamental operational challenge to supplying metals for the energy transition, particularly in developed markets such as the United States that have high levels of transparency and both political and civil society scrutiny of policy," said S&P Global Market Intelligence Executive Director Mohsen Bonakdarpour.

S&P analysts do not see enough cobalt or nickel in the pipeline to meet U.S. clean energy transition demand.

According to the new study on the IRA's impact, this landmark bill signed into law last August is adding an extra 14% growth in America's cobalt demand.

Meeting the IRA domestic or FTA country sourcing requirement will likely be a challenge in a global market where the Democratic Republic of Congo (DRC) accounts for 68% of global mined supply and roughly 70% of the world's cobalt refining happens in China.

While there is enough cobalt produced in free trade agreement countries to meet the IRA domestic sourcing requirement, the U.S. does not currently source most of its cobalt from those countries.

S&P analysis identified enough refined cobalt supply in Canada and Australia to meet America's energy transition supply demands, but most of that cobalt is currently exported to countries that do not have free trade agreements with the U.S.

Redirecting this cobalt to the U.S. at a time when there is intense global competition for this battery metal will be challenging, according to the S&P study.

Finding enough nickel for EV batteries and clean energy storage is expected to be even more challenging. S&P analysts could not find enough nickel supply in free trade agreement countries to meet the added 13% demand increase driven by the IRA – even if all primary nickel production in FTA countries was exported to the U.S.

During 2022, nearly 75% of the world's nickel was mined in China, Indonesia, New Caledonia, Philippines, and Russia – none of which have free trade agreements with the U.S.

As a result, more than 40% of U.S. nickel imports came from non-FTA countries last year, including 11% from Russia.

Even if the U.S. could make a major shift in its nickel supply chains, the S&P study forecasts that America's demand for nickel that meets IRA sourcing requirements will surpass the total supply available in FTA countries by 2030, and the supply gap continues to grow out to 2035.

"Unless there is a significant change in investment, there will not be enough nickel production in FTA countries to meet US domestic sourcing requirements for energy-transition-related technologies, let alone other end-market demand or demand in other FTA countries," S&P Global penned in its report.

Despite the essential role copper plays in the energy transition that the IRA is designed to support, this metal of electrification is neither on the official list of minerals critical to the U.S. nor subject to the same sourcing requirements as the other minerals and metals critical to America's clean energy future.

According to S&P analysis, the demand for copper is expected to double by 2035. The objectives of the IRA itself contribute to 12% copper demand growth over that time.

This demand growth means the U.S. will become more reliant on imports for its copper needs as energy transition-related demand growth outpaces domestic supply.

In its best-case scenario, S&P Global estimates that annual production from global mines will be 1.6 million metric tons (3.5 billion pounds) short of meeting copper demands in 2035. In its most pessimistic view, this copper shortage is a staggering 9.9 million metric tons (21.8 billion lb), according to a report published by the commodities research firm last year.

"The challenge is that if current trends continue ... there's a huge gap," Yergin said upon the release of the copper analysis. "And it's important to recognize that now, not in 2035."

Like the other energy transition metals, this is putting the U.S. in a position where it must compete with other countries with their own energy transition ambitions for an inadequate supply of copper.

"As copper demand increases globally, trade rivalries will intensify – especially if capacity additions cannot keep up with demand," S&P Global penned in its new IRA impact report.

Currently, the U.S. relies on Chile, which happens to be an FTA country, for 60% of its refined copper imports. For Chile, however, the U.S. accounts for only 20% of its refined copper exports. America's largest competitor for Chilean copper is China, which buys more than 40% of the copper shipped from this South American nation.

"As demand increases globally and copper markets tighten, China has a better bargaining position than the US to secure Chilean supply, meaning the United States may struggle to secure enough supply to meet growing energy transition demand," according to the S&P report.

The U.S. could circumvent global energy transition competition challenges and meet the IRA sourcing criteria by producing its energy transition metal needs at home. One homegrown issue, however, stands in the way – an extraordinarily long permitting timeline.

Yergin talked about this issue in detail during a keynote address at the Alaska Sustainable Energy conference convened by Alaska Gov. Mike Dunleavy in May.

"Our country is suffering from a permitting pandemic – it leads to paralysis, lack of economic resolve, and a great deal of pain," the S&P Global Vice Chairman told the audience.

U.S. Deputy Secretary of Energy Dave Turk, who also delivered a keynote address at the Alaska energy conference, agrees with Yergin's analysis that the often decade-long wait for federal authorizations for mining projects hampers America's competitiveness.

"If we are going to be successful in this competition and if we are going to take advantage of these opportunities, the jobs, we need to permit much, much quicker than we do right now," he said.

When you add in the time it takes for federal and state authorizations, inevitable litigation, and then development, it can often take the better part of two decades to go from permit applications to producing the first metal at a mine in the U.S.

"So, if we started today, we are talking about the 2040s to get something done," said Yergin.

This timeline falls outside of the Biden administration's ambitious climate goals that include having EVs make up 50% of all vehicle sales in the U.S. by 2030 and the nation achieving net-zero greenhouse gas emissions by no later than 2050.

S&P says that if permitting timelines were streamlined, copper represents a particularly robust opportunity for the U.S.

The analytical firm has identified more than 70 million tons of an untapped copper endowment on American soil, equivalent to more than 20 years of U.S. copper demand, even at the level of peak energy transition-related requirements in 2035.

The five largest copper projects not yet in operation account for more than 54% of the 70 million metric tons of copper in the U.S. deposits identified by S&P.

Solving the permitting pandemic, however, will be key to getting these and other domestic energy metals projects across the finish line in time to fill the demand being powered by the IRA.

"Expediting permitting reform while meeting environmental and community concerns has become a central topic in boosting mineral supply for the energy transition," said S&P Global Market Intelligence's Mohsen.

With more than 16 years of covering mining, Shane is renowned for his insights and and in-depth analysis of mining, mineral exploration and technology metals.

Reader Comments(0)