The Elements of Innovation Discovered

The Elements of Innovation Discovered

Metal Tech News - July 28, 2023

Nearly $1 trillion needs to be invested in the lithium batteries powering the energy transition, including heavy investments in the mining sector feeding raw materials into the supply chain.

Benchmark Minerals Intelligence cautions that the gigafactories being erected around the world will be "about as useful as grain silos" unless hundreds of billions of dollars are invested in ensuring that there are plentiful supplies of the cobalt, graphite, lithium, manganese, nickel, and other raw materials these factories require to manufacture the lithium batteries powering the electric vehicle revolution.

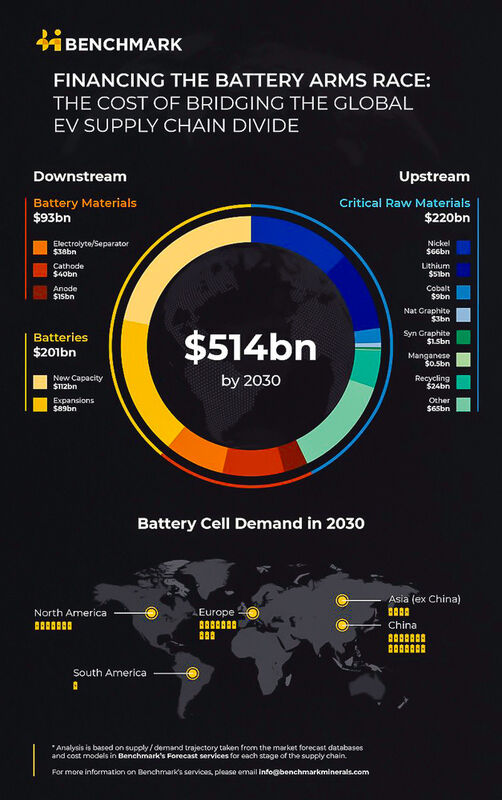

The foremost lithium battery supply chain analytical firm calculates that at least $514 billion is needed across the entire supply chain to meet expected demand in 2030, and $920 billion by 2035.

At more than 40%, the largest portion of this investment needs to be put toward producing the raw materials that will go into the 3.7 terawatt-hours of lithium batteries that are forecast to be produced by 2030, which is up from the current 1 TWh currently being produced.

And the battery supply chain is a relatively small but integral part of the larger mineral-intensive energy transition that requires a roughly $35 trillion cash infusion by 2030, according to the International Renewable Energy Agency.

"The energy transition is still in its early stages and massive capital deployment is going to be needed in order to meet the goals of industry and policy makers," said Benchmark Mineral Intelligence COO Andrew Miller. "Energy storage might form a relatively small piece of the overall financing required, but it is a strategically critical piece of the puzzle. Batteries are the platform technology for clean energy goals, so financing these supply chains is at the heart of the race towards net-zero."

Investments into the mining, refining, and recycling of battery materials need to be made sooner rather than later.

"A gigafactory can be built in two to five years. A refinery can be built in two. But the mines needed upstream of them take between five and 25 years to develop," Benchmark penned in a recent briefing on the cost of bridging the global EV supply chain divide.

Benchmark Mineral Intelligence CEO Simon Moores says the energy transition is highlighting the importance of mining, a sector that forms the first link in essentially every global supply chain but is far removed from products minerals and metals are made from.

"That's the hardest job in the industry – it's a thankless task for the prospectors, developers and pioneers that actually go around the world and look for these minerals and put in the real hard work to actually attempt to bring them to production," he said during the opening address of Benchmark's Battery Gigafactories USA 2023 conference held in Washington, DC.

"It's the hardest job in the supply chain but it's absolutely all eyes on that sector now, and it's deserved," he continued.

When it comes to the batteries that will power the EVs and store the clean but intermittent electricity generated by wind and solar, Benchmark calculates that $220 billion will need to be allocated toward this sector endeavoring to feed minerals and metals into the lithium battery supply chain.

"Lithium-ion batteries and electric vehicles are an industrial pillar of the 21st century and they are the center point of this energy transition," Moores said. "The critical mineral supply chains that fuel these industries are as geopolitically important as the oil pipelines of today and in the agendas of governments they are above that industry – that's how important it's got."

Benchmark says the largest critical battery material supply investments need to go toward boosting the supply of lithium and nickel, which account for more than half of the estimated $220 million required investment.

"Benchmark's view is that lithium, more than any other part of the supply chain, will be the bottleneck for the growth of the battery industry," the firm inked in its lithium battery supply chain brief.

Based on its analysis, Benchmark forecasts that more will be needed in 2030 alone than was mined globally between 2015 and 2022.

The company estimates that $51 billion needs to be invested in lithium over the next six years.

While lithium has the biggest risk of bottlenecks, an even larger investment of $66 billion needs to be made in nickel before the end of the decade.

Unlike lithium, which had very little market demand before the advent of the lithium battery, the nickel supply chain is better established.

Most of the world's nickel is currently used for non-battery applications, with stainless steel accounting for half of global nickel demand in 2030. Batteries, however, are the fastest-growing market for nickel and are expected to account for 32% of global demand for this alloy and battery metal by 2030.

Benchmark also foresees shortfalls of graphite, the single largest ingredient in today's lithium-ion batteries, by the end of the decade, but the investments needed to bridge this gap are smaller.

"Natural and synthetic graphite are forecast by Benchmark to have a combined supply gap of 3.6 million tonnes (metric tons), but the relatively lower capital requirements for graphite mines and synthetic graphite production facilities results in an investment need of $4.3 billion," the firm wrote.

Benchmark says investments also need to be made into cobalt, manganese, and recycling to bridge the "great raw materials disconnect."

"A disconnect where the mine supply is going about half the pace of battery EV demand. And that gap is going to take a long time to bridge, it's going to take more than this decade to bridge," Moores said.

With more than 16 years of covering mining, Shane is renowned for his insights and and in-depth analysis of mining, mineral exploration and technology metals.

Reader Comments(0)